By: Alex Ferrante; Jennifer Vogt, PhD; and Stuart Yasgur, PhD

Today, the U.S. housing market is characterized by rising costs, declining affordability, and limited accessibility. This has made the prospect of owning a home seem more like a distant dream than a goal that can be achieved. With the price of homes and rents outpacing wages, millions are caught in a cycle of cost burden. As housing becomes more unaffordable, access to ownership is restricted for many.

Housing affordability and availability have long been persistent challenges. The conventional solution? Build more homes. But if increasing supply were the answer, why is housing production slowing down in the areas with the highest demand, while prices continue to climb? Economic theory suggests that supply should shift outward to meet demand, but in many cases, this is not happening. One reason for this is that there are politically designed constraints, such as zoning, preventing supply from moving freely.

Acknowledging these constraints is an important step, and recent work has raised awareness of the role they play in limiting access to housing (Hanley, 2023; Kazis, 2020). However, focusing on removing these constraints may not offer meaningful improvements in the long term. To understand why, we need to dig deeper and look at the root causes of the affordability crisis. To do this, it will be instructive to look to the framework developed by Nobel Laureate Amartya Sen in his seminal work on famines (Sen, 1981).

Sen showed that contrary to the widely held belief, famines can occur when there is little change in the aggregate supply of food. Rather, famines occur when political, social, and economic institutions make it difficult for people to access food, even when it exists. Sen famously said, “Starvation is a matter of some people not having enough food to eat, and not a matter of there being not enough food to eat.” What he means is that famines can happen even when there is adequate food production, but people don’t have the resources or rights to access the food, which he defines as “entitlement failures”. According to Sen, such failures arise from political choices that materialize through legal barriers and their enforcement.

Sen helps us see that famines, long thought to be caused by supply shortages, actually result from entitlements failures, when barriers to access have been created and maintained through political choice. In their 2024 paper, McClure and Schwartz make a similar observation about housing. Their findings suggest that the stock of housing in the U.S. is broadly adequate, yet there is a distinct misalignment between income and housing prices. What looks like a shortage of homes is, in reality, an affordability and entitlement failure problem.

The parallels suggest it is worth asking: is the U.S. experiencing a housing famine?

To be clear, nothing in this question is intended to understate or in any way diminish the reality of human suffering that comes with famines. Rather, the point is to explore whether Sen’s analysis may shed light on the current housing crisis; and, if so, can it help point to more effective remedies.

Does the parallel hold? Is the U.S. is experiencing a housing famine? Are political choices enacting legal barriers to homeownership that create entitlement failures which result in housing insecurity and homeownership shortage?

Policies such as exclusionary zoning laws limit where new homes can be built, and financial requirements like 20% down payments restrict who can buy. These are not mutually beneficial arrangements, they reflect political choices that, over time, have determined who is entitled to housing and who is excluded. This is part of a long history. For instance, the Federal Housing Administration (FHA), established by the National Housing Act of 1934, helped millions of Americans purchase homes. But it also systematically excluded African American communities through redlining and the refusal to insure mortgages in predominantly Black neighborhoods. These policies not only limited homeownership for these communities but also cemented wealth disparities that persist today. The FHA’s actions are an example of how political decisions expanded housing access for some, while systematically denying entitlements for others.

The question remains, if current politically designed constraints like zoning systematically deny entitlements to prospective homeowners, why shouldn’t we think that changing zoning laws alone would help address the supply problem?

To answer this, we need to go one step further and ask where these constraints came from in the first place. As noted, housing restrictions are not arbitrary, they are the outcome of political choices shaped by special interest groups over time. Mancur Olson’s theory of special interest groups helps us make sense of this dynamic. In his work, The Rise and Decline of Nations, Olson suggests that small, organized groups with concentrated interests will lobby for policies that protect their position, even when these policies impose welfare costs on the broader public.

This pattern is clearly visible in the housing market. Historically, landlords and homeowners formed powerful coalitions to ensure that policies such as zoning, building codes, and land use regulations would secure the value of their property and limit competition from new supply. These arrangements did not just regulate land use, they ensured that housing would become a vehicle for wealth preservation.

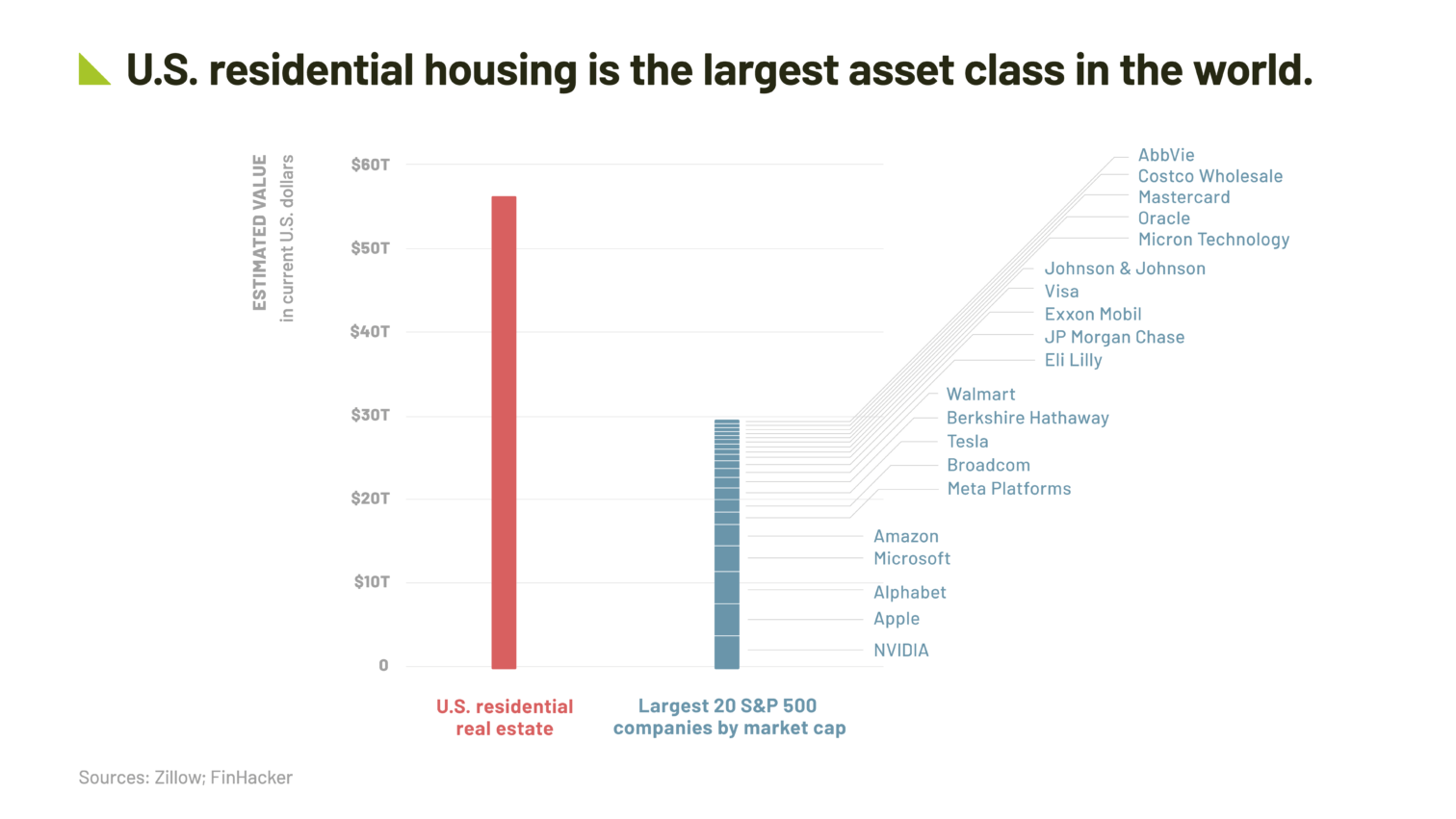

Today, the legacy of these political choices is evident in our housing market’s structure. Residential homes in the U.S is one of the largest asset class globally, estimated to be valued at over $50 trillion. This extraordinary concentration of wealth is not a coincidence; it is the cumulative outcome of political choices designed to make homeownership an appreciating asset. Thus, understanding supply constraints requires that we recognize how the political choices of powerful interest groups have shaped housing policy to protect wealth stored in housing. This concentration of wealth is an essential element of the housing famine.

Homeowners have a clear, and reasonable, interest in continued appreciation. Housing is a store of wealth for homeowners. Rising home values build personal wealth. It also reinforces the perception that real estate is a wise investment, which contributes to further price increases. One important consequence of this is that homeowners have an interest in the returns from housing rising faster than the returns from labor. If returns from labor exceed returns on housing, capital would shift away from housing as a store of wealth and towards investments tied to returns on labor. This would lead to a decrease in housing prices and the erosion of the wealth stored in housing.

As a result, there is a direct conflict of interest between those who rely on ownership of housing to build wealth (homeowners) and those who rely on returns from labor (non-owners or renters).

If returns on labor trail the returns from housing, then it will continue to get harder and harder for renters to become homeowners. And, if homes were to become more affordable for renters, then this would mean that returns from labor exceed returns from housing, and it would lead to a decrease in housing prices and the wealth stored in housing.

Given the magnitude of the housing market, $44 trillion plus all the other assets and financial mechanisms tied to the housing market, when the interests of homeowners and renters are weighed against each other, all too often, the balance will tip towards homeowners. Unfortunately, this is happening in decisions large and small across the country. Barriers to entry for renters and non-owners continue to grow, resulting in entitlement failures.

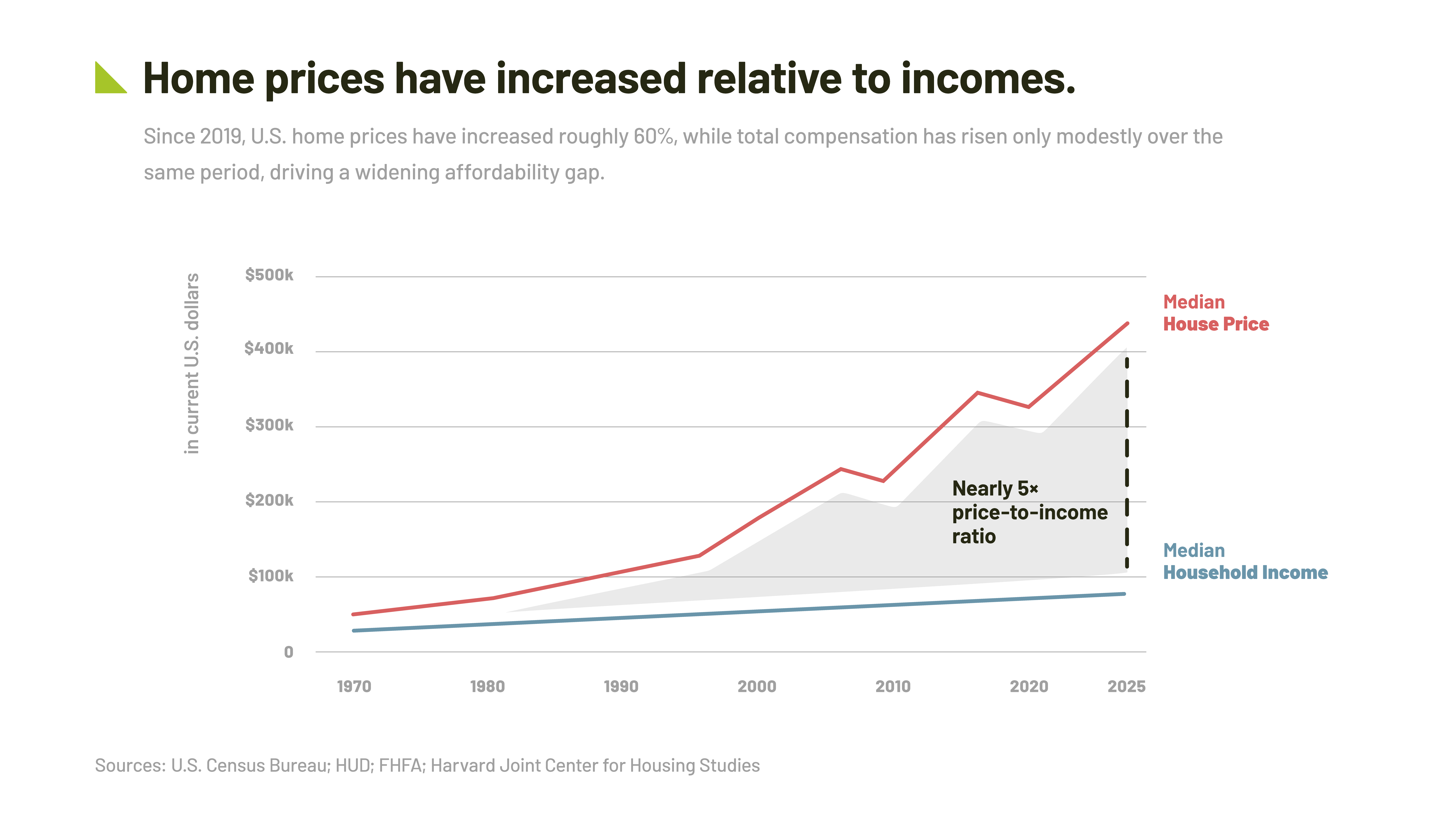

This is exactly what we see in the data. Nearly half of Americans believe that the availability of affordable homes is a major concern where they live (Schaeffer, 2022). Between late 2019 and 2024, U.S. home prices rose by roughly 60% (Harvard JCHS, 2025). Over the same period, real total compensation grew by about 1.8% per year (Edelberg and Steinmetz-Sibler, 2025). Compounded over roughly five years, that amounts to total compensation growth of only about 10–11%—far short of the increase in home prices. This rapid increase in home prices, combined with much slower income growth, has created significant financial strain. In 2023, cost-burdened homeowner households increased by roughly 646,000, reaching about 20.3 million – nearly one-quarter of all homeowners (Harvard JCHS, 2025).

The conflict of interests between homeowners and renters is at the heart of the housing famine. So long as housing wealth continues to appreciate at a rate far exceeding the growth of wages, non-homeowners will face compounding entitlement failures. Each year of rising property values without commensurate labor returns widens the entry barrier, effectively trapping renters in a cycle where saving for ownership becomes increasingly out of reach. This dynamic ensures that non-homeowners are pushed further away precisely because of the system’s design to reward existing owners. Without structural changes to realign the returns to housing and labor, millions of households will remain locked out of ownership, perpetuating scarcity and deepening the famine in housing access.

As mentioned, homeowners have acted as a powerful lobby, successfully protecting their wealth through political decisions guided by asset incentives. The interests of homeowners to protect their property value has resulted in legal constraints on supply, causing some housing markets to suffer from limited growth. In fact, in some coastal cities, the relationship between high prices and new construction has weakened or even reversed (Glaeser and Gyourko, 2025). High-demand areas are seeing dramatic declines in new buildings, particularly in low-density, high-price neighborhoods. This is precisely what Olson’s theory predicts – constraints designed to protect special interest groups will eventually lead to a slowing in economic growth.

Understanding that there is a housing famine helps us see the underlying causes. It allows us to better recognize how politically designed regulations act as a mechanism for suppressing supply. Zoning is one such example. The regulation of land development through zoning laws creates legal constraint, which impacts development potential and supply, often in areas with high demand. By limiting what can be built, zoning laws protect the interests of those who benefit from rising home prices, but it is only one of many mechanisms that perpetuate the famine.

To see the implications of zoning more clearly, consider what happens when these restrictions are reversed. In 2018, Minneapolis became the first U.S. city to eliminate single-family zoning in an attempt to improve housing affordability. A recent study suggests that this reform reduced home prices by 16–34% and rents by 17.5–34% relative to comparable metropolitan areas without such zoning changes (Gu and Munro, 2025). At face value, these are encouraging signs of improvements in affordability. Yet, the same study also finds no significant increase in new construction or housing supply. In other words, home prices and rent fell not because more housing was being built, but because demand was faltering, likely reflecting uncertainty in future expectations as to whether homes will be an appreciating asset.

This outcome suggests that reforming zoning alone cannot resolve the housing famine if the underlying political and financial incentives remain misaligned. Without addressing the broader perception that housing is a productive store of wealth, loosening zoning could simply shift opportunities toward those already positioned to capitalize on lower entry prices. True reform requires more than deregulation. It demands a realignment of interests so that policy decisions promote broad access and shared prosperity.

The famine analogy invites us to look beyond surface-level economics. It allows us to confront the root causes of the housing crisis and approach potential remedies from a new, more insightful perspective. As Amartya Sen demonstrated, famines don’t just occur when food is scarce. They arise when entitlement systems, such as political, legal, and social institutions, determine who can access what already exists. The limited supply of housing in today’s market is not a natural outcome of economic forces, but the result of political choices that have restricted access. Recognizing this reframes the problem from an inevitable market failure to a matter of collective responsibility. It suggests that reversing the housing famine is not only possible but depends on democratic action and a willingness to acknowledge our moral obligation in addressing the deprivation that has been systematically built.

To effectively address the housing famine, we must tackle its underlying cause. Specifically, the conflict of interest between renters and homeowners that results from using homes as a primary store of wealth in society. In fact, this is a specific instance of a more general principle. We should avoid using essential goods, such as housing, as vehicles for wealth accumulation. As long as we use homes as a primary store of wealth, we can expect to have a growing entitlement failure, making homeownership increasingly difficult for those who rely on returns from labor to build wealth.

To resolve the conflict of interests at the heart of the housing crisis, society must begin to transition toward alternative stores of wealth. There are two possible areas of focus that can resolve this conflict. The first is reducing the role of housing as a store of wealth. The second is developing alternative vehicles for wealth building that are accessible to homeowners and renters alike.

Reducing the role of housing as a store of wealth must be done with care. Sudden disruptions could destabilize the housing market or unintentionally erode the value of existing assets in a way that creates more harm than good. One fruitful approach may be to increase the relative number of homes that do not act as a store of wealth.

Promising examples of this already exist. Community Land Trusts (CLTs) separate ownership of the land from ownership of the home. This limits the capital appreciation of the home. As a result, CLT homes are not vehicles for building wealth through capital appreciation. But they can be very effective for building wealth in other ways. The limited capital appreciation of CLT homes means that they have lower prices. As a result, CLT home purchase and ownership can be more affordable. This leaves more income for building wealth in other ways.

CLTs are a model that have proven to work well and are growing in popularity across the country. They create a number of additional benefits as well. Increasing the number of CLTs is one way we can increase affordable housing while also reducing the role of housing as a store of wealth.

The second area of focus is developing vehicles for wealth building that are accessible to homeowners and renters alike.

This is an area that is ripe for innovation. Not only does it have the potential to avoid the conflict between homeowners and renters, but it also has the potential to increase the ability of renters to build wealth and is an opportunity to increase economic productivity. After all, storing wealth in the walls of people’s homes is not a particularly productive use of an enormous amount of capital. This could also be in the interest of large financial institutions and capital allocators, who would be involved in offering the new wealth building products.

Recognizing that the U.S. is in a housing famine helps us understand that approaches that fail to resolve the conflict between homeowners and renters are less likely to be successful. These efforts might be beneficial for other purposes (e.g., improving the supply chain or helping specific groups become homeowners), but they are unlikely to materially affect the housing crisis.

The challenge, then, is not to eliminate wealth creation through housing, but to redesign the system such that the pursuit of wealth generates broad social benefit rather than deepening inequality.

Addressing the housing famine will require structural innovations – updated institutional arrangements that align incentives and distribute gains more equitably.

As housing innovation continues to evolve, there is a significant opportunity to develop new structures of ownership that are less reliant on housing as a store of wealth. These models would unhinge housing from wealth accumulation and create more sustainable, inclusive pathways to homeownership, where individuals and communities can benefit without contributing to the rising tide of inequality. By reimagining how we think about ownership and wealth-building, we can create a housing system that is both accessible and productive, working for the betterment of society.

Understanding that the housing crisis shares critical features with Sen’s analysis of famines enables us to uncover the deeper, underlying problems that have fueled the crisis. This perspective allows us to diagnose the root causes more clearly, align interests that drive political decisions, and develop meaningful, long-term solutions. By recognizing that the U.S. is experiencing a housing famine, we shift toward structural innovations that prioritize accessibility and sustainability, that ultimately increase society’s productive capacity. Through this reframing, we can make the dream of homeownership a reality again for millions of Americans.

References:

Edelberg, W., & Steinmetz-Sibler, N. (2025). Has pay kept up with inflation? Brookings Institution. https://www.brookings.edu/articles/has-pay-kept-up-with-inflation/

Glaeser, E., & Gyourko, J. (2025). America’s housing affordability crisis and the decline of housing supply (Brookings Papers on Economic Activity, Conference Draft). Brookings Institution. https://www.brookings.edu/articles/americas-housing-affordability-crisis-and-the-decline-of-housing-supply/

Gu, H., & Munro, D. (2025). Zoning reforms and housing affordability: Evidence from the Minneapolis 2040 Plan. SSRN Working Paper. https://doi.org/10.2139/ssrn.5347083

Hanley, A. (2023). Rethinking zoning to increase affordable housing. Journal of Housing and Community Development. https://www.nahro.org/journal_article/rethinking-zoning-to-increase-affordable-housing/

Harvard University Joint Center for Housing Studies. (2025). The state of the nation’s housing 2025. https://www.jchs.harvard.edu/state-nations-housing-2025

Kazis, N. (2020). Ending exclusionary zoning in New York City’s suburbs. Furman Center. https://furmancenter.org/research/publication/ending-exclusionary-zoning-in-new-york-city8217s-suburbs

Manhertz, T. (2025). U.S. Housing Market Value Hits $55.1 Trillion. Zillow Research. https://www.zillow.com/research/housing-market-value-1-trillion-35518/

McClure, K., & Schwartz, A. (2025). Where is the housing shortage? Housing Policy Debate, 35(1), 49–63. https://doi.org/10.1080/10511482.2024.2334011

Olson, M. (1982). The rise and decline of nations: Economic growth, stagflation, and social rigidities. Yale University Press. http://www.jstor.org/stable/j.ctt1nprdd

Schaeffer, K. (2022). Key facts about housing affordability in the U.S. Pew Research Center. https://www.pewresearch.org/short-reads/2022/03/23/key-facts-about-housing-affordability-in-the-u-s/

Sen, A. (1983). Poverty and famines: An essay on entitlement and deprivation. Oxford University Press. https://doi.org/10.1093/0198284632.001.0001